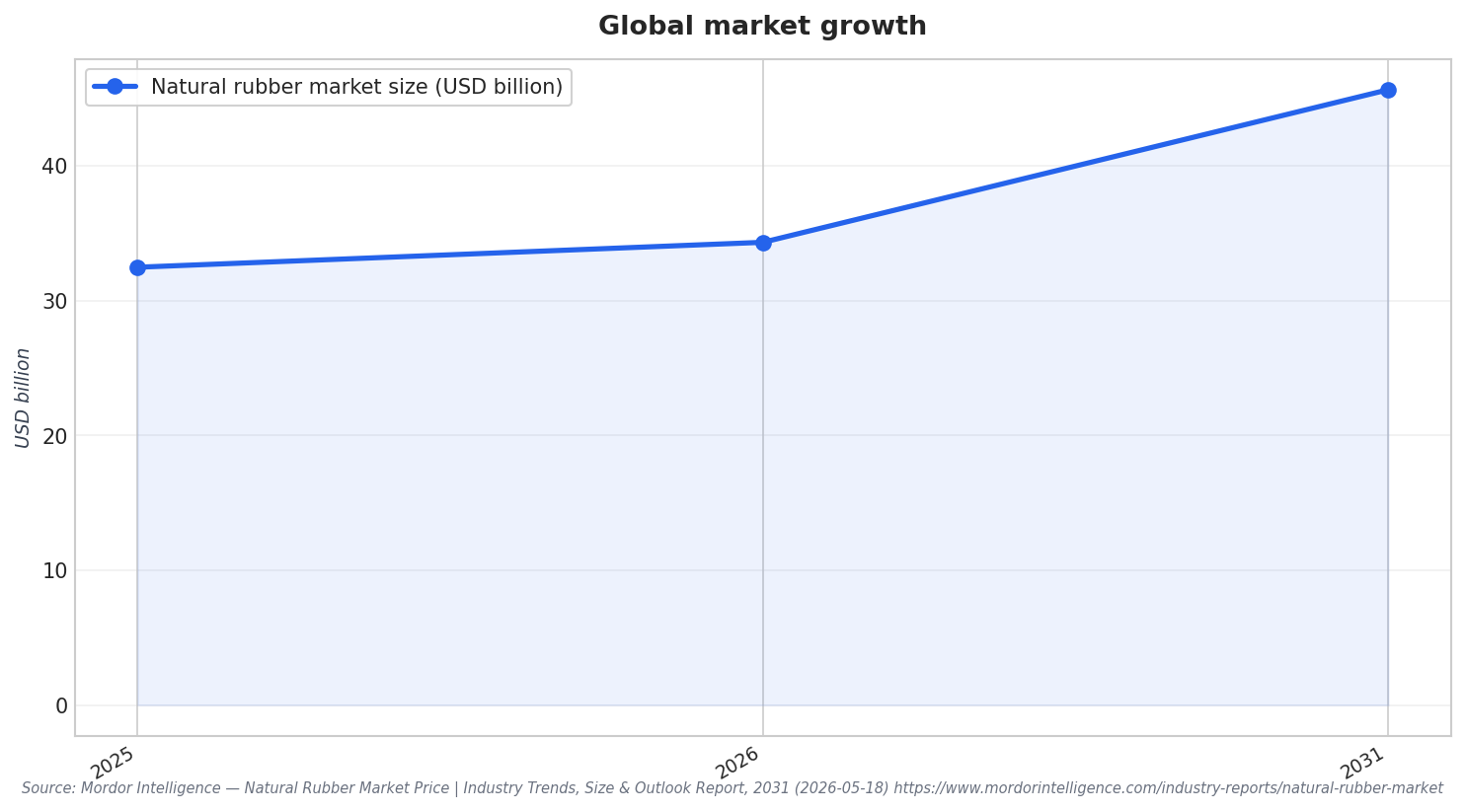

Global fundamentals are creating a supportive backdrop for higher natural rubber prices. In 2026, global production is forecast at 15.2 million metric tons versus demand of 15.6 million metric tons, leaving a 0.4 million metric ton gap, according to the Association of Natural Rubber Producing Countries as cited by Mordor Intelligence. That gap matters for Thailand because Asia-Pacific is both the leading production hub and the leading demand center. Mordor Intelligence also estimates Asia-Pacific held 67.8% of the natural rubber market share in 2025, reinforcing how regional constraints can quickly turn into global price support.

Within that regional picture, Thailand’s scale is repeatedly highlighted as a key factor in supply sensitivity. A Thailand-focused statistics compilation describes a production ecosystem spanning 3.9 million hectares and 1.7 million households, with around 800 million trees tapped. It also frames Thailand as deeply connected to global supply chains, particularly to downstream manufacturing in China. Research published on ScienceDirect adds that Thai rubber prices are influenced by international markets and have shown sharp fluctuations over the past seven years across different market levels, underscoring why shifts in global supply balance can translate quickly into domestic price moves.

Why Supply Tightness Persists in 2026

Multiple sources point to constraints that limit rapid supply responses. Mordor Intelligence cites adverse weather, limited replanting, weak smallholder productivity, land-use shifts, and leaf fall disease as factors that can keep supply tight. Expert Market Research adds an important seasonal dynamic for Thailand and Indonesia: during the wintering period from January to March, trees shed leaves and latex yields drop significantly, which can tighten availability, especially if it coincides with inventory building by Chinese tire manufacturers. It also notes disease pressure in Thailand’s northeastern plantation zones from Lasiodiplodia theobromae leaf blight, adding another layer of yield risk.

Demand-side context helps explain why these supply constraints matter. Expert Market Research estimates that in 2024 the Asia-Pacific region consumed nearly 12 million metric tons of natural rubber, a 0.6% growth after two consecutive years of decline. It also states Asia-Pacific accounts for approximately 92% of global natural rubber supply, concentrating the price impact of any disruption in major origins. For policy, it notes that the International Tripartite Rubber Council (Thailand, Indonesia, and Malaysia) has historically deployed coordinated supply management measures, including the Agreed Export Tonnage Scheme (AETS), to stabilize prices during sustained downturns.

Thailand’s own market outlook shows how these global forces can translate into local revenue expectations. Grand View Research estimates the Thailand rubber market generated USD 785.7 million in 2024 and is expected to reach USD 1,018.7 million by 2030, with a projected CAGR of 4.4% from 2025 to 2030. It also reports Thailand accounted for 1.6% of the global rubber market in 2024 and that natural rubber was the largest revenue-generating type segment that year. In practice, that means the Thailand natural rubber industry is exposed to both tighter global supply conditions and evolving trade requirements such as traceability and auditable sourcing systems referenced by Mordor Intelligence.

What is driving tighter global natural rubber supply in 2026?

How large is Thailand’s rubber production ecosystem?

What seasonal factor can tighten Thailand’s rubber supply?

What is the outlook for Thailand’s rubber market revenue?

What does the Thailand natural rubber industry’s price history suggest about volatility?