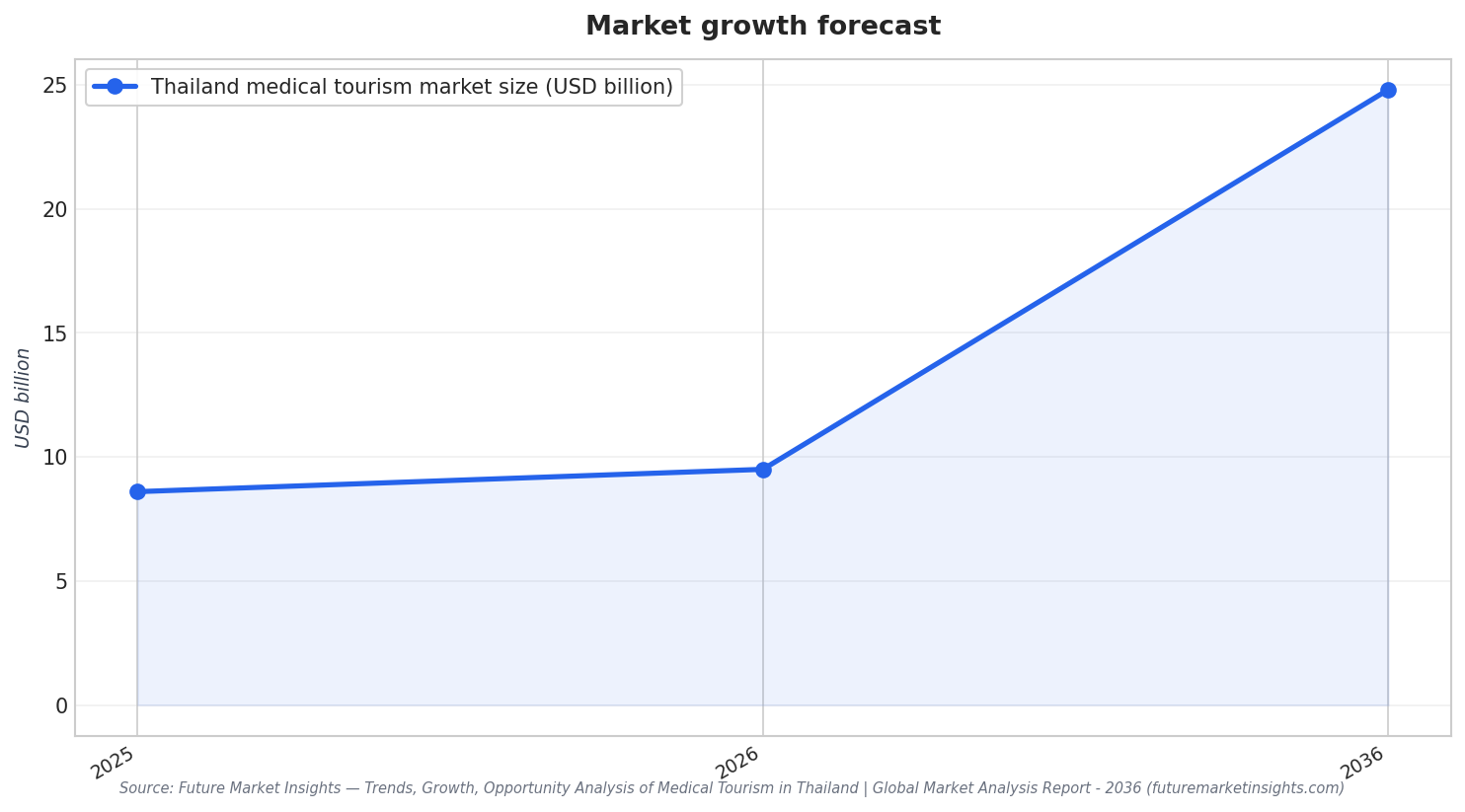

Thailand medical tourism is increasingly framed around value and outcomes, not just price. Future Market Insights (FMI) estimates the country’s medical tourism industry generated USD 8.6 billion in 2025, with projections of USD 9.5 billion in 2026 and USD 24.8 billion by 2036, at a 10.1% CAGR (2026–2036). The same outlook describes a transition away from a predominantly cost-driven elective model toward a higher-value hub focused on complex, high-acuity treatments. That shift is also tied to rising demand for oncology services, robotic-assisted surgeries, and other technologically advanced interventions that raise average revenue per patient and support a value-over-volume approach.

Cost still matters, but it is becoming a gateway rather than the whole proposition. FMI notes cost advantages of 40–70% compared with Western healthcare systems as a demand driver, while Ken Research states average procedure costs in Thailand are 50–70% lower than in the U.S. The U.S. Commercial Service adds that an average medical tourist can expect to save 25% to 75% on various procedures and treatment options. Yet the market narrative is changing: FMI links growth to insurers and government payers prioritizing accredited outcomes over baseline savings. That encourages providers to compete on clinical capability, technology, and standardized quality rather than simply attracting volume through low prices.

From Electives to Complex Care: Who Benefits and Where

Segment signals show both continuity and acceleration. FMI’s breakdown cited in an openPR release puts cosmetic surgery at a 25% share in 2026, and private hospitals as the dominant service provider with a 70% share. But the same source emphasizes faster growth in higher-value categories such as cardiology, orthopedics, and fertility treatments due to technological advancements. Nexdigm’s market view also points to a broader, more specialized case mix, segmenting demand across oncology, neurosurgery and spine surgery, dental, ENT, gynecology, urology, ophthalmology, and plastic and reconstructive surgeries. In that report, oncology holds the largest share, supported by advanced cancer care infrastructure and specialized oncologists, reinforcing the move toward more complex care pathways.

Quality infrastructure is a central pillar of the value shift. Nexdigm reports 62 hospitals accredited by Joint Commission International (JCI) across Thailand, while the U.S. Commercial Service reports 59 JCI-accredited Thai medical institutes as of August 2023, offering services ranging from organ transplants to dental and cosmetic surgery. The same U.S. source cites Thailand ranking 5th out of 46 destinations in the 2020–2021 Medical Tourism Index. On the provider side, FMI cites BDMS reporting an 11% increase in international patient revenue in 2024, driven by high-complexity cases from Qatar and China. TRIS Rating credit analysts also noted in November 2025 that stronger revenue growth from patients from Europe, the Middle East, Myanmar, China, and other countries could mitigate a near-term decline in Cambodian patient volume.

Geography and project development also reflect higher-value positioning. FMI identifies Bangkok and Phuket as primary hubs, and the openPR summary highlights Bangkok as a top growth hub at 12.5% CAGR. The U.S. Commercial Service reports a government plan to turn Phuket into a world-class medical tourism hub by 2028, including an international complex called “Medical Plaza.” The project includes a one-stop medical center operated by Vachira Phuket Hospital and a 5,000-capacity multipurpose convention center, with construction of the medical center expected to finish by 2026. The planned services—geriatric and palliative care, physical therapy and rehabilitation, and international healthcare—align with a shift toward longer-stay, higher-acuity care models rather than quick elective procedures alone.

What is driving the shift in Thailand’s medical tourism from low-cost to high-value care?

How large is Thailand’s medical tourism market expected to be over time?

Which treatment and provider segments lead in Thailand’s medical travel sector?

What evidence suggests international patients are increasingly seeking complex care in Thailand?

What developments are planned for Phuket as a medical hub?