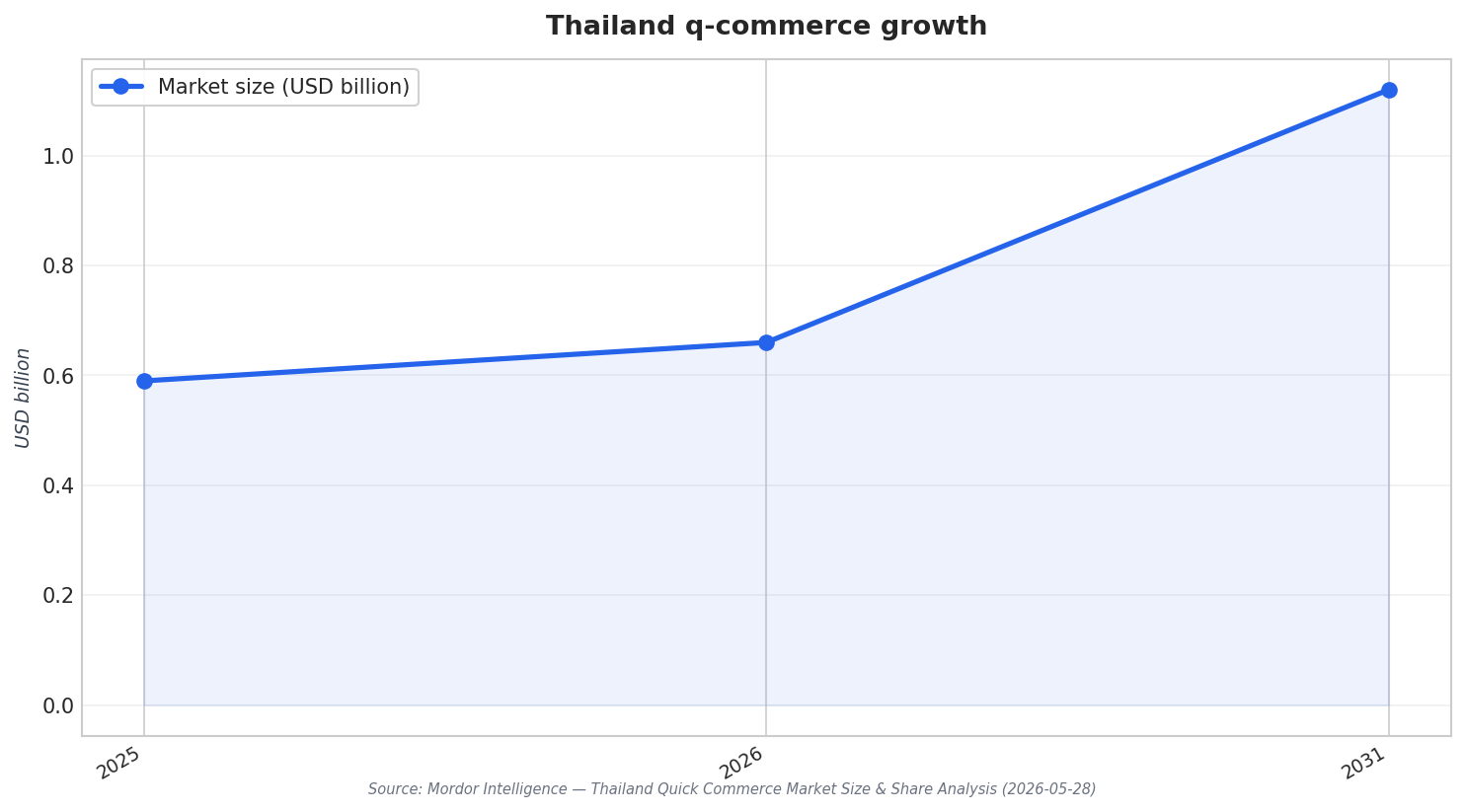

Thailand quick commerce is reshaping how urban shoppers buy groceries, staples, and everyday items. Mordor Intelligence values the country’s quick-commerce market at USD 0.59 billion in 2025 and estimates it grows from USD 0.66 billion in 2026 to USD 1.12 billion by 2031, at a CAGR of 11.25% for 2026–2031. ResearchAndMarkets’ databook also projects expansion, forecasting the market rises from US$385.0 million in 2024 to about US$630.2 million by 2029, with a CAGR of 10.3% from 2025 to 2029. Across sources, the direction is consistent: rapid delivery is becoming a standard way to buy small, frequent baskets in dense cities.

In Thailand, the category mix signals that rapid delivery is no longer just about meals. Mordor Intelligence reports Grocery and Staples held 53.48% of the quick-commerce market share in 2025. That aligns with a broader retail baseline: Technavio values Thailand’s grocery segment at USD 95.76 billion in 2024 within the wider retail market. The quick-commerce angle is the shift from planned stock-up trips toward repeat ordering for staples, health-related purchases, and other daily-use items, as platforms broaden beyond restaurant delivery. This widening mix gives operators more levers to build basket value while still optimizing for fast order cycles.

Why Speed Is Getting More Reliable in Bangkok and Urban Clusters

Delivery-time promises are tightening as networks thicken in Bangkok and nearby urban clusters. Mordor Intelligence finds the 11–30-minute promise accounted for 56.25% of market share in 2025, while “less than 10 minutes” is projected to grow at an 11.77% CAGR through 2031. The infrastructure underpinning this model is also digital. Thailand recorded 4G population coverage at 98% and active mobile broadband subscriptions at 122 per 100 inhabitants, according to the International Telecommunication Union dashboard cited in the Mordor report. This matters because quick commerce depends on app-led ordering, location tracking, instant confirmation, and continuous rider communication.

Platform structure is also shaping how quick commerce scales locally. ResearchAndMarkets notes Thailand’s ecosystem is dominated by multi-service platforms such as LINE MAN Wongnai, Grab, and Robinhood, which expanded from food delivery into groceries, convenience items, and pharmacy products. Instead of relying primarily on dark stores, the same source says growth is anchored in hybrid models that leverage store networks from 7-Eleven, Lotus, Big C, and Tops. Among retailers, 7-Eleven (CP All) is described as dominating store-based quick commerce via its “7-Delivery” app, followed by Lotus’s Go Fresh, Big C Online, and Tops Online. It is also a consolidating market, with Foodpanda’s exit in 2025 reducing international competition.

As this channel matures, competition is expected to shift from aggressive price tactics toward execution. ResearchAndMarkets says the next 2–4 years should bring more consolidation around ecosystem anchors, with expansion focused on operational efficiency, integration with digital payments, and sustainability-led logistics. Mordor Intelligence similarly argues smaller entrants face tougher entry conditions because scaled platforms and large retailers already control rider density, app traffic, and store-based fulfillment points. For urban grocery and retail delivery, the practical outcome is clear: consumers get more dependable short windows, while brands and retailers must win on availability, fulfillment speed, and seamless app experiences rather than novelty.

How big is Thailand’s quick-commerce market, according to the sources?

Which product category leads quick commerce in Thailand?

What delivery window is most common in Thailand’s quick-commerce market?

Who are the major players shaping rapid grocery delivery in Thailand?

What is driving the growth of Thailand quick commerce in cities?