Thailand industrial real estate demand is being pulled by a mix of factory relocation, policy clarity, and the gravitational pull of the Eastern Economic Corridor (EEC). Developers listed in Bangkok are also shifting toward logistics and industrial assets in the EEC, where demand links to e-commerce and data center investments, according to Mordor Intelligence. That pivot is happening alongside a wider market backdrop where Thailand’s real estate market size is estimated at USD 60.78 billion in 2026 and is expected to reach USD 80.00 billion by 2031, with a 5.65% CAGR during 2026 to 2031 (Mordor Intelligence). The corridor story matters because it concentrates investment attention into a few provinces, where land availability, infrastructure, and incentives can move decisions quickly.

In Q1 2026, Colliers Thailand reported that the industrial estate market absorbed 1,914 rai of industrial land, up 16.70% year over year, and the occupancy rate rose to 82.55%. The pattern was unusually compressed, with more than 70% of ownership transfers (35 out of 50 deals) occurring in March alone. Colliers linked the acceleration to three converging triggers: new BOI investment promotion measures announced in January 2026 and extended until end-2027, US tariff policy developments around February 20–21, 2026 that included a 15% global import tariff, and a February 28, 2026 closure of the Strait of Hormuz that pushed cargo insurance premiums up four to six times while diversions extended delivery times by 10 to 15 days. Together, these factors reinforced how quickly land commitments can surge when manufacturers try to lock in costs and reduce uncertainty.

Why the EEC Is the Pressure Point for Land, Supply, and Pricing

Supply is rising, but it is also becoming more concentrated in the EEC. Colliers reported Thailand had 213,941 rai of allocated industrial estate land at the end of Q1 2026, with net leasable and saleable area at 143,251 rai, up 6.29% from a year earlier. New supply entering the market totalled 4,369 rai, all located in the EEC and delivered through phased expansions of existing estates, with no new greenfield industrial estate projects launched in the period. Even with around 24,900 rai of vacant land noted by Colliers, the location and readiness of sites still shape what manufacturers can use quickly. This is why expansions inside established estates can matter more than headline land availability.

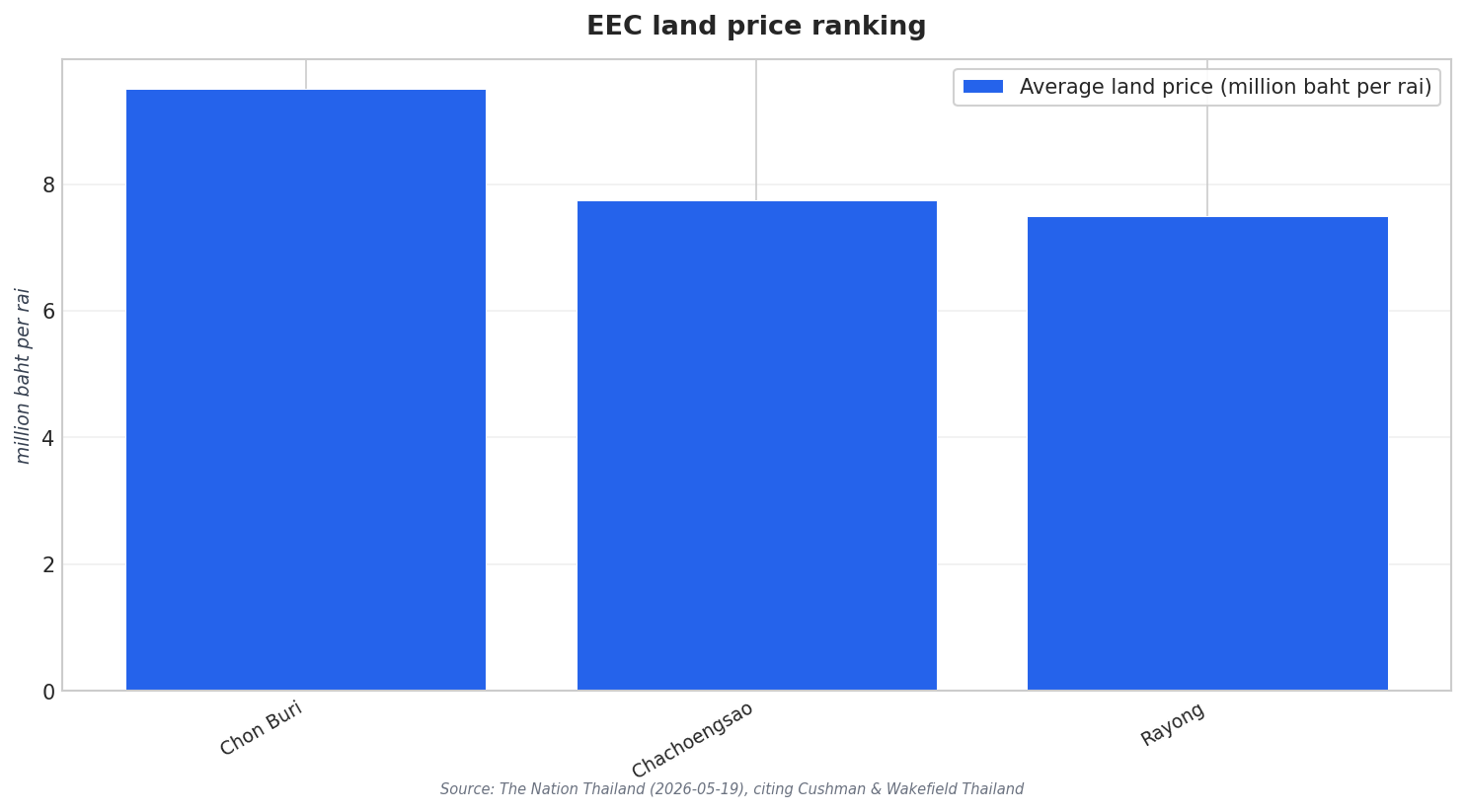

Pricing signals show tightening in high-demand locations, especially where foreign capital is active. Cushman & Wakefield Thailand said land prices in Chon Buri and Rayong rose by 20–30% over the past two years, driven by Chinese investors buying land inside and outside industrial estates. In the EEC, average prices were cited at 9.5 million baht per rai in Chon Buri, 7.75 million baht per rai in Chachoengsao, and 7.5 million baht per rai in Rayong, while the industrial land vacancy rate fell to 6.2%. Separately, Mordor Intelligence reported industrial land values reached USD 169,000 per rai in H1 2024, up 17% year over year, and linked the trend to relocation from China amid trade-war drag. These figures help explain why competition is intensifying for serviced plots near ports, roads, and established supplier ecosystems.

Not every industrial format is tightening at the same speed, which is important for occupiers comparing land purchase with ready-built options. Cushman & Wakefield Thailand reported that ready-built factory space remained unchanged from the end of last year at 3.42 million square metres, but the vacancy rate increased to 10.57% from 9.53%, suggesting absorption is not keeping up with available space. At the same time, JLL said warehouse demand remained strong in Q4 2025, with Eastern Vicinity leading built-to-suit activity and the EEC recording absorption of existing stock. On the demand-side ecosystem, LWS reported that Amata City Chonburi has a formal workforce of more than 200,000 people, and that the EEC has cumulative condominium supply of more than 15,000 units, with some locations posting rental occupancy above 90% and rental yields of 5–7% a year. That workforce-and-housing linkage reinforces why industrial location decisions in the EEC can become long-term commitments rather than short, speculative moves.

What is driving Thailand’s industrial estate land absorption in early 2026?

How concentrated is new industrial land supply in the EEC?

What pricing and vacancy signals stand out in the EEC industrial land market?

What is happening in the ready-built factory segment?

How does Thailand’s industrial real estate outlook connect to the EEC’s workforce demand?