Thailand’s grid strategy is tightening around one priority: flexibility. As of April 2025, Thailand had approximately 52 GW of total installed power generating capacity, with renewable energy at around 20% of that total installed capacity. The Royal Thai Government is developing the 2024-2037 National Energy Plan (NEP), planned for release by end-2025, and the Power Development Plan (PDP) within it is expected to raise the share of renewable energy in total electricity generation to 51%, up from 36% under PDP 2018. That shift is paired with a clear direction: integrate energy storage systems into the energy mix so solar and wind can expand without undermining grid stability.

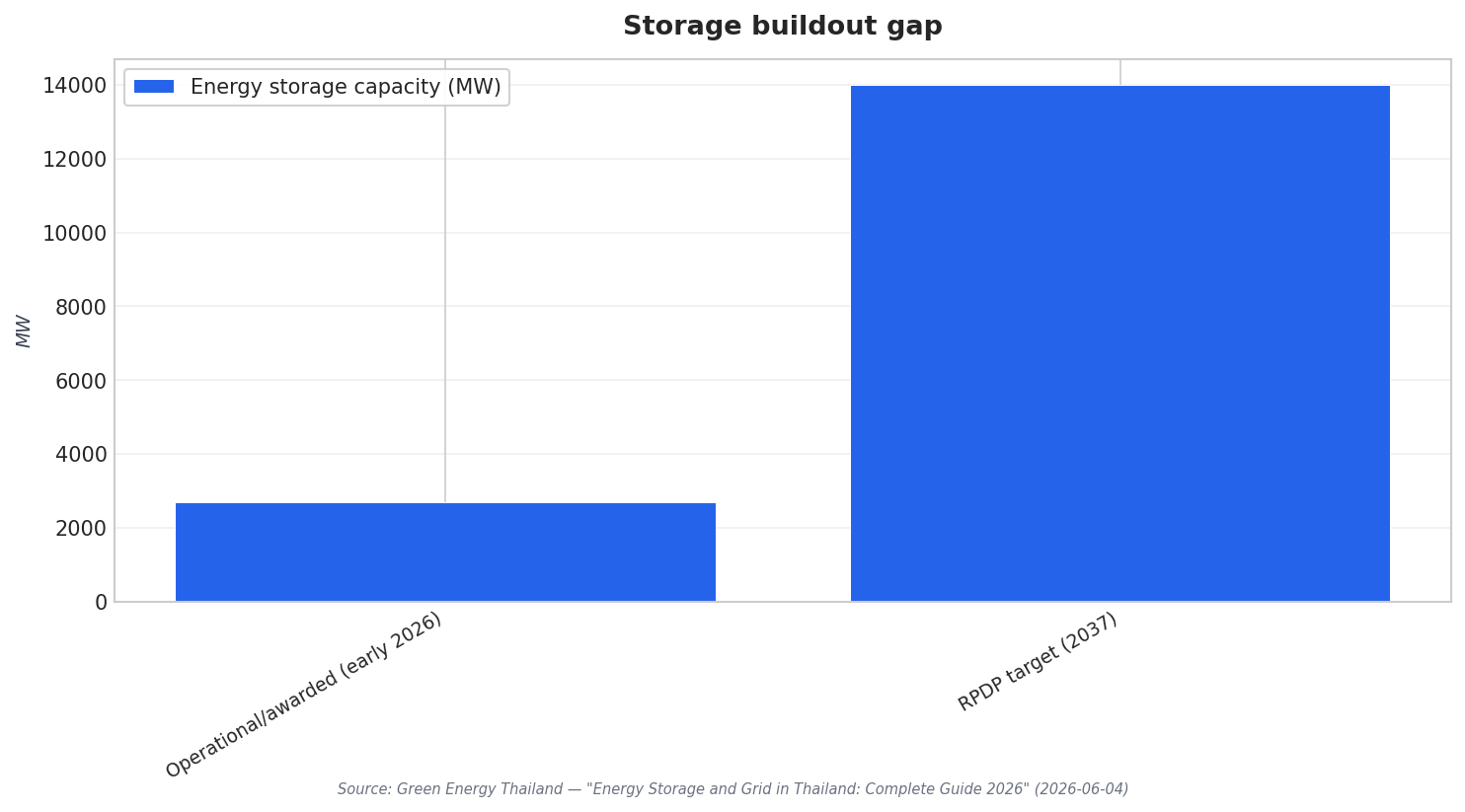

The near-term storage pipeline already signals momentum, even if it is far from complete. Thailand’s Renewable Power Development Plan (RPDP) targets 14 GW of energy storage by 2037 to support a grid running on 51% renewable electricity. As of early 2026, the country has roughly 2,685 MW of storage capacity operational or awarded, described as 19% of the way to that 2037 target. Utility experience is also building: EGAT operates 42 MW / 43 MWh of grid-scale BESS across three sites—Bamnet Narong (16 MW), Chai Badan (21 MW), and Mae Hong Son (5 MW)—positioned for frequency regulation and renewable integration rather than bulk shifting.

Why Storage Economics and Grid Planning Are Converging

Policy and planning are increasingly designed to reward dispatchable renewables, not just installed capacity. Thailand’s incentive structure explicitly differentiates solar with storage from stand-alone solar. Solar-plus-BESS projects receive 2.8331 THB/kWh compared to 2.1679 THB/kWh for stand-alone solar, a 31% premium. At the same time, grid constraints are shaping where and how storage is deployed. A 2022 feed-in-tariff (FiT) auction awarded 5 GW across solar, wind, and battery projects, but southern congestion has delayed roughly 500 MW of grid connections, highlighting the need to pair generation growth with transmission and balancing resources.

Market signals also point to a rising role for hybrid systems and modernization spending. Thailand installed nearly 3 GW of solar PV capacity in 2024, lifting cumulative solar capacity to 11.875 GW. EGAT’s floating-solar roadmap spans nine reservoirs totaling more than 2,700 MW, supporting faster tie-ins via existing hydro grid nodes. Meanwhile, grid modernization outlays of THB 90 billion (approximately USD 2.6 billion) are described for pumped-storage dams and high-voltage corridors, underlining the system-wide need for flexibility. MarkWide Research also flags battery-wind hybridization in southern wind assets and notes transmission congestion in the Central region as a factor that can delay commissioning and affect dispatch outcomes.

These forces are visible in the commercial outlook for the Thailand energy storage market. Data Bridge Market Research values Thailand’s Battery Energy Storage System market at USD 2.97 billion in 2024 and projects it to reach USD 10.58 billion by 2032, with a 17.30% CAGR from 2025 to 2032. In 2024, on-grid (grid-tied) systems accounted for USD 2.32 billion in revenue, and residential is listed with USD 1.13 billion in 2024 while also identified as the fastest-growing application at a 17.72% CAGR through 2032. In ASEAN context, Mordor Intelligence expects the ASEAN energy storage market to reach USD 3.55 billion in 2025 and USD 4.92 billion by 2030, and it notes that countries including Thailand are leading adoption, with a focus on industrial applications and renewable integration.

What is Thailand targeting for energy storage by 2037?

How much storage capacity is operational or awarded in Thailand as of early 2026?

How do tariffs support solar paired with batteries in Thailand?

What is the outlook for the Thailand energy storage market through 2032?

What grid-scale battery projects has EGAT already deployed?