Thailand’s rooftop solar sector is moving into a faster lane after a coordinated 2026 policy shift that combines fiscal incentives, regulatory reform, and targeted initiatives. Dentons describes the change as a decisive push to accelerate rooftop adoption and an overhaul of the solar rooftop framework that is among the most significant in over a decade. The near-term backdrop is a market that had built strong fundamentals, but saw progress slow in more recent years, even as the country kept expanding solar more broadly. The new approach is designed to remove friction for projects and improve the investment case for households and companies that want more control over electricity costs and supply.

Measured against the national solar base, rooftops are already material. TransitionZero reports that rooftop solar accounted for 35% of total installed solar capacity as of late 2023, reaching 1.77 GWp, citing DEDE. EnergyTracker also puts the rooftop share at 35% of total installed solar capacity in 2023 and adds that residential installations increased by 32% year over year. However, TransitionZero and EnergyTracker both note that Thailand’s overall capacity growth has been relatively flat compared with some regional peers, which is why the new policy package matters: it targets faster deployment from the “grassroots level upward,” in TransitionZero’s framing.

What the 2026 Tax Incentive Reform Changes for Households

A key 2026 lever is household tax relief tied to real-world project completion and grid connection. Junno Energy reports that residents who install rooftop solar are eligible for a personal income tax deduction of up to 200,000 baht, applicable to projects where payment is completed and the system is connected to the grid between 2026 and 2028. That incentive lands in a market where residential growth is already accelerating: Mordor Intelligence forecasts residential rooftops advancing at a 10.25% CAGR, the fastest pace among end-user categories in its Thailand solar energy market view. Mordor also notes that simplified licensing for systems below 1 MW and solar leasing models are helping drive a residential installation boom in Bangkok and peri-urban provinces.

Economics are reinforcing the policy story. Mordor Intelligence states module prices fell to USD 0.10–0.12 per watt in 2024, which trimmed commercial payback periods to five to seven years and enhanced bankability across customer classes. It also reports retail tariffs at THB 4.15–4.18 per kWh in 2024, while the Electricity Generating Authority of Thailand reported cumulative losses of nearly THB 98 billion, suggesting an 8–12% tariff hike by late 2025 is likely. In that environment, Mordor says manufacturers in the Eastern Economic Corridor increasingly view rooftop solar as a hedge, with a typical 1 MW installation paying for itself within seven years.

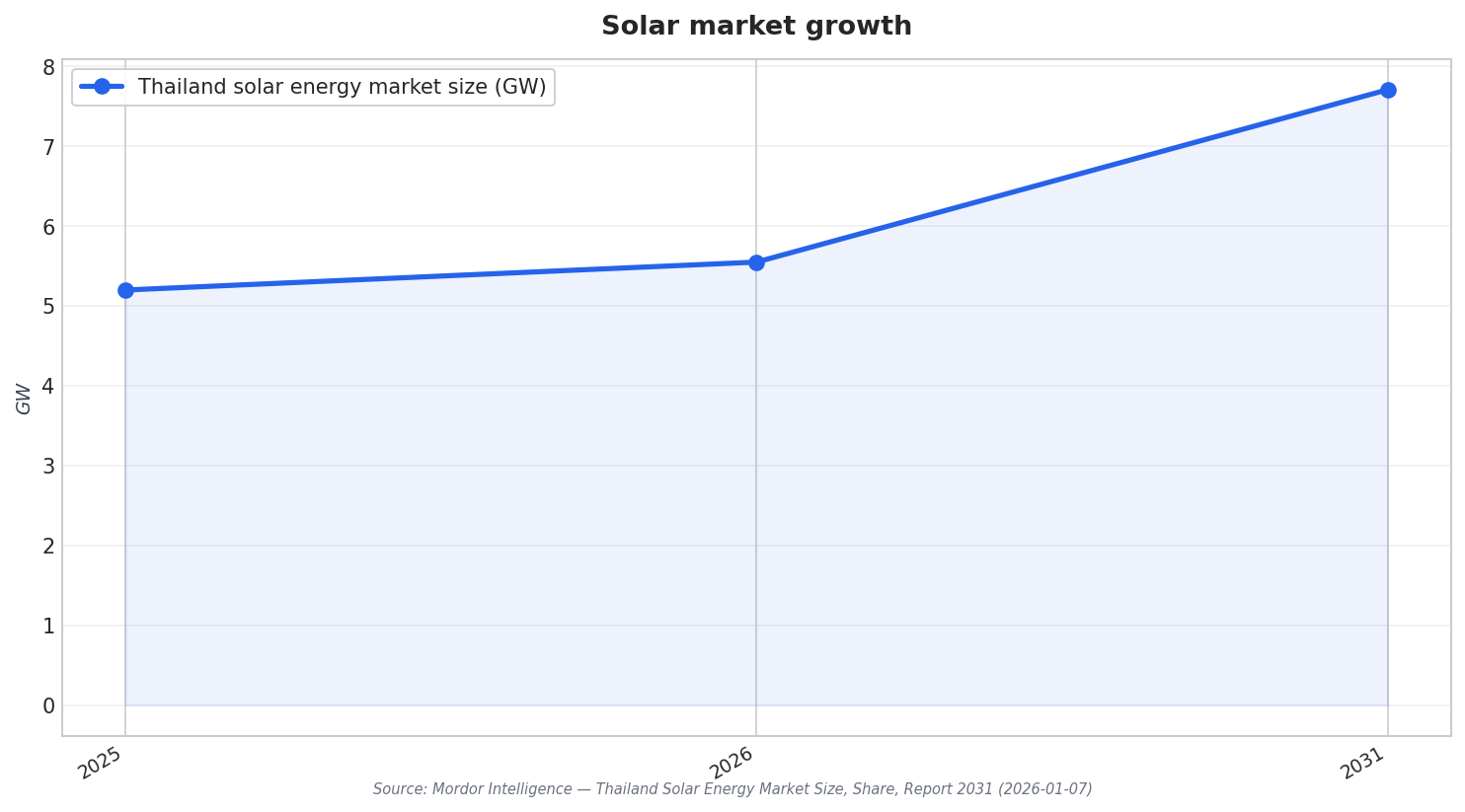

Looking ahead, the broader solar pipeline signals momentum that rooftops can ride. Junno Energy projects new solar PV installed capacity reaching 1.2–1.8 GW in 2026 and says commercial and industrial distributed solar, particularly rooftop systems, represents about 36% of the market, while large ground-mounted plants make up over 60%. Mordor Intelligence expects Thailand’s solar energy market size to grow from 5.20 GW in 2025 to 5.55 GW in 2026, reaching 7.71 GW by 2031, and highlights a 2,000 MW direct power purchase pilot approved in 2024 that opens an alternative procurement path for data centers and large manufacturers. Together, these forces help explain why the Thailand rooftop solar market is poised to accelerate after the 2026 incentive and legal reset.

What is the 2026 rooftop solar tax incentive in Thailand?

How big was rooftop solar in Thailand by late 2023?

What is driving payback improvements for commercial rooftop PV?

How does the Thailand rooftop solar market connect to electricity tariff trends?

What does 2026 look like for overall solar additions in Thailand?